US Initial Jobless Claims – Preview – 01.10.25

We have benchmarked the release against prior 218k and consensus / street 223k, and frame the call using the most recent high-frequency labor and activity signals (claims trend, continuing claims, JOLTS, ADP, ISM/S&P PMIs), plus known data quirks (early-September state-level fraud distortions) and seasonal effects around quarter-end.

The objective is to set a base case, define a realistic surprise range, and map market implications, while acknowledging operational risks to publication timing.

![]()

What the Latest Data Suggests – As of Today, Wed 01 Oct

-

Claims trend: After a fraud-driven spike (TX) to 264K in early September, claims normalized to 231K (w/e Sep 13) and 218K (w/e Sep 20). Continuing claims stayed elevated at 1.926m (w/e Sep 13), consistent with slower rehiring, not a surge in layoffs.

-

Hiring flow: JOLTS (Aug) showed openings 7.227m (+19k) but hiring fell to 5.126m, quits eased, a picture of soft demand and weak hiring rather than rising layoffs.

-

High-freq labor checks today: ADP Sep came in around +52K private jobs (very soft). That keeps the “weak hiring, low layoffs” story intact for claims.

-

Activity gauges today: ISM Manufacturing (Sep) printed around 49.0 (still contraction), but S&P Global’s final manufacturing PMI sits near 52.0. Net: industry is mixed / sluggish, not collapse, again, not the kind of shock that usually spikes claims week-to-week.

US Initial Jobless Claims – Our Call vs Consensus

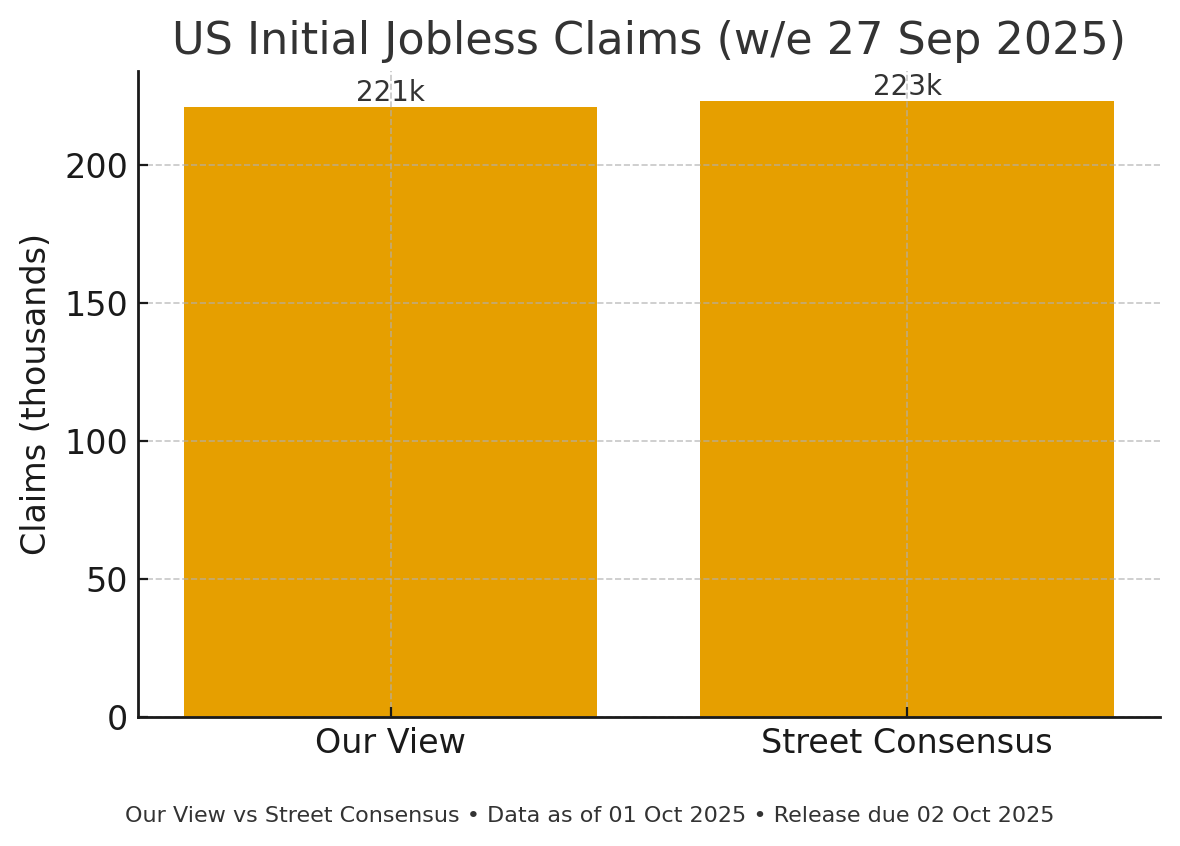

Base case: 221K (vs consensus/street 223K).

68% “most likely” range between: 217K–226K.

Why a hair below consensus?

-

The Texas identity-fraud bulge appears fully washed out, and the subsequent two prints show return to low-220s.

-

JOLTS & ADP both flag weak hiring, but layoffs stay contained, which tends to anchor initial claims near recent levels rather than push higher.

-

Continuing claims are high, evidence of slower re-employment, but that’s a stock variable; it doesn’t automatically lift new claims week-to-week.

Risks to Our Call:

-

Upside surprise (>230K): If seasonal factors misfire around quarter-end / school-year transitions, or if any state backlogs clear at once.

-

Downside surprise (<215K): Further unwind of early-Sep distortions and ongoing layoff restraint (firms hoarding labor even in a soft patch).

Market take – FX & Rates

-

Claims ≤215K: knee-jerk USD bid, front-end yields up; USDJPY pops, EURUSD dips.

-

Claims ~220–225K (my base): Muted reaction; focus stays on shutdown headlines and Friday data risk (if published).

-

Claims ≥230K: USD offered, front-end yields down; EURUSD firmer, USDJPY soggier.

Two contextual drivers for Thursday:

-

Shutdown mechanics: DOL has said weekly claims would not be released during a shutdown. If the standoff persists into Thursday, markets will trade proxies (ADP, ISM details, claims whispers) instead of the official print.

-

Macro tone: The dollar has already softened on shutdown risk and mixed labor reads; rate-cut odds for October have risen, amplifying sensitivity to any downside claims surprise.

Bottom line

-

Expectation: 221K — a touch below consensus 223K.

-

Bias: More risk of small downside than upside given the recent re-normalization and lack of fresh layoff signals.

-

Caveat: Publication is at risk due to the shutdown; if it’s paused, use ADP (~+52K) and ISM employment commentary as the stop-gaps for labor tone.

If you want, I can add a quick trade plan grid (levels & triggers) for EURUSD / USDJPY / GBPUSD around three outcomes (≤215K, 216–229K, ≥230K).

Conclusion

Our base case is 221k (range 217k–226k), modestly below consensus (223k), reflecting contained layoffs after the early-September distortion washed out and a labor market that is softening via weaker hiring, not rising separations. A downside miss (<215k) would likely elicit a knee-jerk USD bid and front-end selloff; an upside surprise (>230k) would do the opposite, though the bar for a lasting trend move is high without corroboration from broader labor prints. If the official release is delayed, the labor tone should be proxied with ADP and survey employment components, but our directional bias remains: claims anchored in the low-220s with slightly greater risk of a small downside surprise than an upside break.

For similar Forex Markets news please visit our Markets News page.

Please visit our Disclaimer page.

Disclaimer

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these or any financial instrument or instruments.

TerraBullMarkets.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets or any financial instrument involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress.

All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of TerraBullMarkets.com nor any of its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

TerraBullMarkets.com and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. TerraBullMarkets.com and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and TerraBullMarkets.com are not registered investment advisors and nothing in this article is intended to be investment advice.