ISM Manufacturing PMI Preview: Upside Surprise Risk Builds Ahead of Monday’s US Factory Data

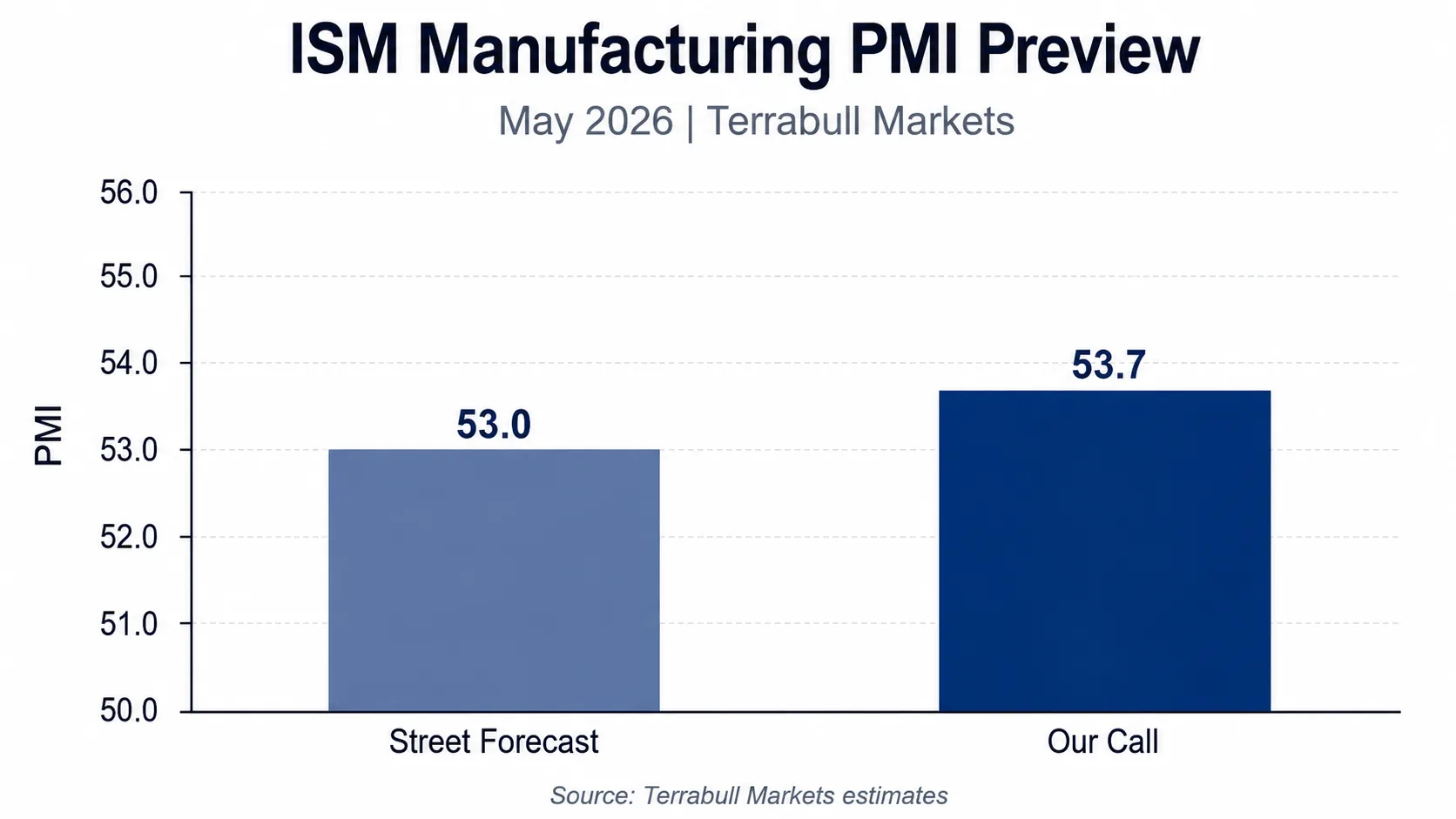

The next major US macro test arrives on Monday 1 June 2026 at 15:00 UK time, with the release of the May ISM Manufacturing PMI and the accompanying ISM Manufacturing Employment Index. The street is looking for a broadly stable manufacturing print, with consensus around 52.6 and forecast at 53.0, following April’s 52.7 reading.

Our call is more constructive. We expect the headline ISM Manufacturing PMI to print closer to 53.7, implying a moderate but meaningful upside surprise versus consensus. For the employment component, we expect a smaller improvement to 47.1, still below the 50 expansion threshold but firmer than April’s 46.4.

Base case – Our Call vs Street Estimates

| Series | Prev | Cons./Street | Our Call | Surprise skew |

|---|---|---|---|---|

| ISM Manufacturing PMI (May) | 52.7 | 52.6 | 53.7 | Above street forecasts of 53 and consensus of 52.6 |

| ISM Employment | 46.4 | 46.6 (street forecast) | 47.1 | Mild Upside, still contractionary |

Why We See Upside Risk

The strongest argument for an above-consensus print comes from the latest US manufacturing survey. The US Manufacturing PMI rose to 55.3 in May, its strongest in close to four years, while the output component also strengthened materially. All pointing to a manufacturing sector that is not just stabilising, but showing genuine near-term momentum.

Regional manufacturing data also supports the case for a stronger ISM headline. The most striking signal came from the Chicago PMI, which surged to 62.7 from 49.2, a very large one-month swing back into expansion territory. New orders and production were notably strong, showing demand and current activity improved sharply in the Midwest.

The Empire State Manufacturing Survey also surprised positively, with the headline index rising to 19.6, helped by solid new orders and shipments. Richmond Fed manufacturing data added to the constructive picture, with its composite index improving to 13 from 3, and gains across shipments, new orders and employment.

These indicators suggest the market may be underestimating the breadth of May’s manufacturing improvement.

The Key Caveat: Employment Remains the Weak Link

While headline activity looks better than expected, employment remains less convincing. April’s ISM employment component fell to 46.4, indicating contraction in manufacturing payroll conditions. Even with better production and order trends, firms may remain cautious on hiring due to uncertainty around input costs, tariffs, energy prices and external demand.

The mixed regional signals matter here. Some surveys showed stronger employment conditions, but others remained soft or only marginally positive. That is why our employment call is 47.1 rather than a move back above 50. We expect improvement, but not enough to declare a full labour-market recovery within manufacturing.

Market Implications

A headline print near our 53.7 call would likely be interpreted as USD-positive and yield-positive, at least initially. A stronger ISM would support the view that US growth remains resilient, potentially reducing near-term expectations for Fed easing and lifting Treasury yields.

For gold, the reaction could be negative if the data lands as a clean growth-positive surprise. A stronger PMI, especially if accompanied by better new orders and firmer prices, would likely strengthen the dollar and push real-yield pressure higher, both typically bearish for Gold.

For equities, the reaction may be more nuanced. A stronger PMI confirms growth resilience, which is supportive for earnings expectations. However, if bond yields rise sharply on the data, rate-sensitive areas of the market, particularly long-duration technology and NAS100, could face pressure.

The cleanest bullish-USD / bearish-gold outcome would be a headline ISM above 54.0, employment above 48.0, and strong new orders. A more mixed outcome would be a headline beat but weak employment, which could limit the durability of any dollar rally.

What Would Prove Our Call Wrong?

The downside risk is that some of the recent survey strength may reflect short-term inventory building, temporary supply-chain effects, or regional distortions rather than broad-based demand. The Philadelphia Fed survey was notably softer, with current activity and new orders weakening in May.

A print below 52.0 would challenge the current resilience narrative and likely trigger a softer USD/yields reaction, while supporting gold. A reading below 50.0 would be a much larger growth scare, though that is not our base case.

Conclusion

Our base case is for the May ISM Manufacturing PMI to beat expectations, with Our Call at 53.7 versus the street forecast of 53.0 and consensus of 52.6. The balance of evidence from S&P Global, Chicago, Empire State and Richmond manufacturing surveys points to firmer activity than markets are currently pricing.

However, the employment component is likely to remain the weak spot. We expect a modest improvement to 47.1, but still below the expansion threshold.

For markets, the release carries clear upside surprise risk for the US dollar and Treasury yields, with potential downside pressure on Gold if the headline, new orders and prices components confirm a stronger manufacturing impulse.

![]()

For similar Forex Markets news please visit our Markets News page.

Please visit our Disclaimer page.

Disclaimer

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these or any financial instrument or instruments.

TerraBullMarkets.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets or any financial instrument involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress.

All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of TerraBullMarkets.com nor any of its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

TerraBullMarkets.com and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. TerraBullMarkets.com and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and TerraBullMarkets.com are not registered investment advisors and nothing in this article is intended to be investment advice.