US CPI & Initial Weekly Claims Preview – 11/9/2025

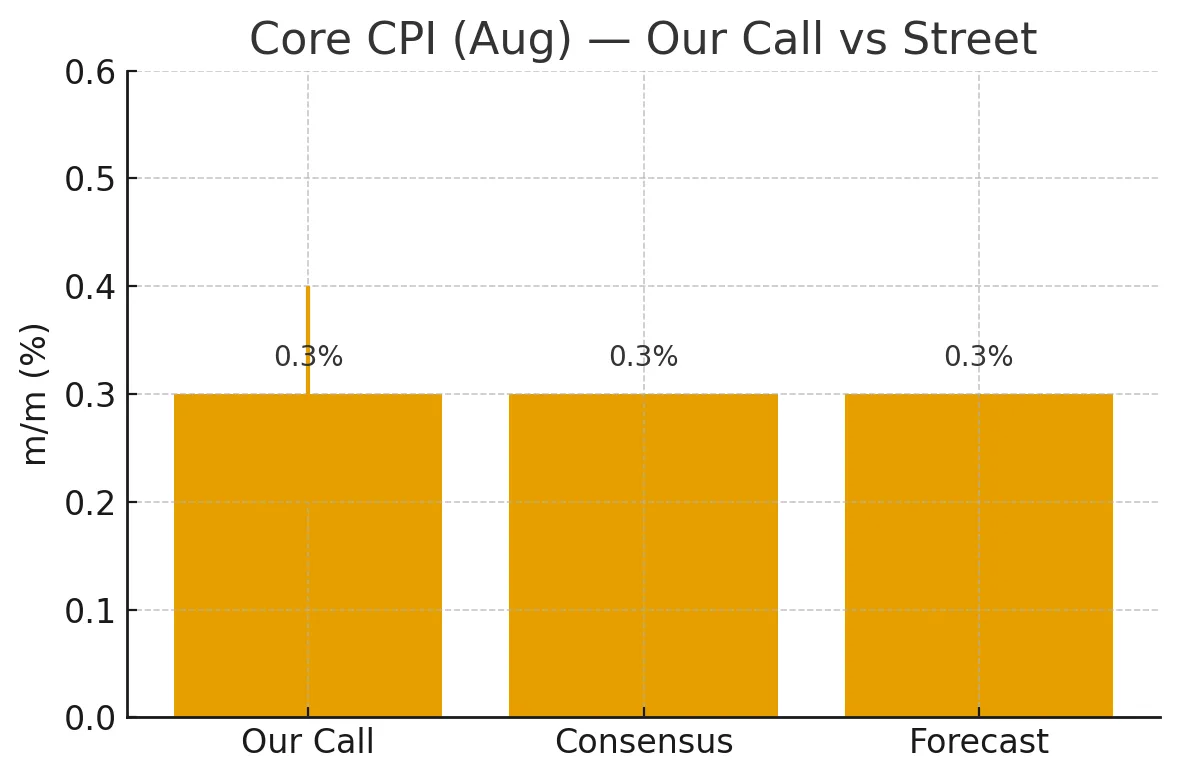

The August CPI lands on Thu 11 Sep, 13:30 UK (08:30 ET) alongside Initial Jobless Claims, setting the tone for front-end rates and the USD ahead of the Fed blackout. The Street is looking for Core CPI +0.3% MoM (3.1% YoY) with the CPI index at 323.9. Our base case is the same.

Sticky services (most notably shelter) offset by soft core goods, with travel categories the being the key swing risk. Claims should remain range bound (235–240k), consistent with a gradually cooling but still resilient labor market. Upside core risk (≥0.4%) would push front-end yields and USD higher. A benign 0.2% core plus softer claims would likely bid Treasuries and leave the USD a touch weaker.

Timing & Setup

- CPI (Aug) is scheduled for 08:30 ET on Thu Sep 11 (13:30 UK).

| Release | Street | Forecast | OUR CALL | Bias |

| Core CPI m/m | 0.30% | 0.30% | 0.30% | tiny downside tail (0.2%) |

| Core CPI y/y | 3.10% | 3.10% | 3.10% | flat |

| CPI index (NSA) | 323.89 | 323.6 | 323.90 | near street |

| Initial Jobless Claims | 235k | 240k | 235–240k (base 237k) | flat-to-slightly higher |

What’s driving the calls:

Energy / headline optics

- EIA weekly shows US regular gasoline averaging $3.15 – $3.19 from late Aug to early Sep; for August CPI the late-month firmness nudges headline higher but is not big enough to force a hot core print.

Core goods

- Used cars: Manheim’s Aug index was unchanged m/m (SA) after a soft mid-month; that usually maps to flat to slightly negative used-car CPI. New-vehicle discounting and softer import prices keep goods disinflation in play.

Shelter

- Forward rent trackers show fresh weakness (Apartment List −0.2% m/m in Aug; y/y −0.9%), which filters into CPI with a lag. Expect rent & OER to decelerate slightly but still add ~0.15–0.20pp to core.

Travel-related services

- July saw a +4.0% pop in airfares; base effects allow partial payback in Aug (even a flat print helps keep core at 0.3%). Hotels have been easing on a trend basis. U.S. Travel Association

Medical & other services

- July’s core lift included medical services; no strong evidence of an August re-acceleration, so assume trend-like contributions. Combined with still-elevated ISM prices paid readings (manufacturing 63.7, services ~69) the services disinflation remains slow, not linear.

Macro context / “why not higher?”

- July CPI was 0.2% headline / 0.3% core, with core y/y = 3.1%; consensus into August is for sticky 3% inflation, echoed by mainstream previews. My base case preserves that profile.

Initial Jobless Claims (week ended Sep 6)

- Latest print was 237k; trend is range-bound, with insured unemployment ~1.94 – 1.95m creeping up vs early-year levels. We pencil in 237k (street 235k; your 240k). A surprise ≥245k would firm the “gradual cooling” labor narrative into next week’s Fed.

What would move markets

- Hawkish inflation surprise: Core ≥0.4% m/m or CPI-U index ≥324.1 → front-end USTs up, USD firmer (watch USD/JPY topside).

- Benign print: Core 0.2%, CPI-U ≤323.8, and claims ≥240k → front-end yields down, USD a bit heavier, mild risk-on.

- Mixed (sticky prices + softer labor): Core 0.3% with claims ≥245k → curve bull-steepens; USD reaction mixed (yields ↓ vs. inflation sticky).

Receipts / references

- CPI schedule & prior index level (Jul NSA 323.048): BLS CPI site & July release.

- Consensus colour: Morningstar preview (CPI +0.3% m/m, sticky inflation narrative).

- Gasoline trend: EIA weekly gasoline update.

- Used-car pipeline: Manheim Aug (flat m/m SA); mid-Aug soft.

- Rents leading indicators: Apartment List Aug report.

- ISM prices paid (cost pressure still elevated): ISM mfg prices 63.7; services prices near high-60s.

- Claims backdrop & last print: Investing/TE trackers.

Latest CPI/Inflation coverage (useful pre‑read)

Bottom line: We stand with consensus—core 0.3% m/m, 3.1% y/y; CPI-U ~323.9—with the main risk a softer outcome if airfares/hotels retrace more and used-car CPI dips. Claims should stay range-bound around ~237k.

For similar Forex Markets news please visit our Markets News page.

Please visit our Disclaimer page.

Disclaimer

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets.

TerraBullMarkets.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets or any financial instrument involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress.

All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of TerraBullMarkets.com nor any of its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

TerraBullMarkets.com and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. TerraBullMarkets.com and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and TerraBullMarkets.com are not registered investment advisors and nothing in this article is intended to be investment advice.