Markets have one eye on inflation, but tomorrow’s US jobs report is the real trigger that could flip the Fed narrative and send rates, the dollar, and risk assets lurching in seconds.

Tomorrow’s US jobs report lands at an awkward moment for markets. Investors are trying to decide whether the US economy is merely cooling toward trend, or if the labor market is finally rolling over in a way that forces the Federal Reserve to pivot sooner than expected. With inflation data published later in the week, the NFP print becomes the first major volatility catalyst, and it is likely to set the tone for rates, the dollar, equities and gold.

Here’s the key framing for markets: the labor market doesn’t need to collapse to move markets.

If hiring slows even modestly below expectations, and unemployment drifts higher, the rate path can reprice quickly, especially if revisions are meaningful.

US NFP Jan Preview – 11th Feb

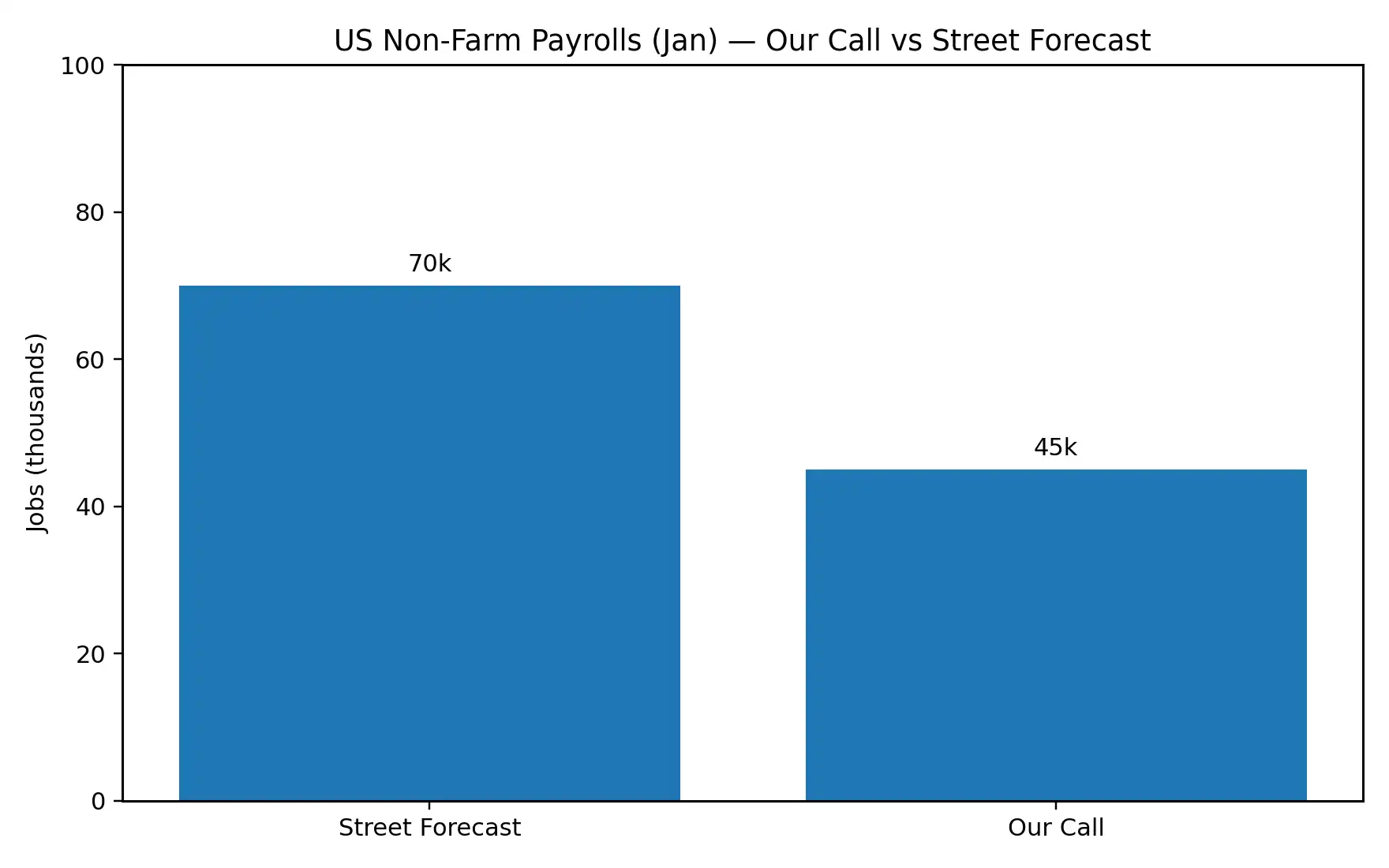

| Data (Jan) | Previous | Street Forecast | Our Call |

| Non-Farm Payrolls (NFP) | 50k | 70k | 45k |

| Unemployment Rate | 4.40% | 4.40% | 4.50% |

In short: we lean softer than consensus on both the hiring number and the unemployment rate, with the biggest surprise risk skewed to the downside on payrolls.

Why Below Consensus: Payrolls

Start with the simplest clue markets watch: the private payroll “pulse.” ADP’s January employment estimate came in at +22k, a very subdued signal compared with what would normally be consistent with a robust headline payroll number.

ADP is not a reliable point-forecast for NFP (the methodologies differ materially), but prints this low tend to coincide with downside risk unless government hiring, seasonal factors or benchmark quirks offset the weakness.

The takeaway isn’t “NFP will equal ADP,” it’s that the hiring impulse looks softer than the street narrative implies.

Next, the labor-market “pressure gauge” from jobless claims. Initial claims were relatively calm through much of late January, but then rose toward 231k for the week ending Jan 31 in many trackers, with reporting often citing weather and seasonal noise.

Continuing claims have hovered around the high-1.8 million area in recent weeks, levels that are not recessionary, but consistent with a market that is no longer tight enough to generate rapid wage acceleration without productivity help.

This backdrop supports a “low fire, slowing hire” story: the economy is still functioning, but employers are not scrambling for labor in the way they were a year or two ago.

JOLTS job openings have also drifted lower toward multi-year lows, and that matters because openings often lead payrolls with a lag. If openings are falling, the next step is usually a slower hiring pace, not necessarily mass layoffs.

The ISM Manufacturing PMI rebounded strongly, but the employment component has often struggled to sustain above 50 during late-cycle slowdowns.

Unemployment: Why a 4.5% Risk

Unemployment is derived from the household survey, which can diverge from the establishment payroll survey, sometimes materially. In a cooling phase, the unemployment rate often rises, not because layoffs spike, but because hiring slows and the “job-finding rate” softens. With openings lower and claims no longer printing “ultra-tight,” a 0.1% uptick to 4.5% is a reasonable base-case risk.

Importantly, the market reaction can be nonlinear: an unemployment rate that stays at 4.4% can allow traders to look through a soft headline payroll print; but if unemployment ticks higher, it adds weight to the “labor market cooling” narrative and tends to pull yields lower faster.

Revisions

One underappreciated feature of many jobs reports at this point in the year is the presence (or proximity) of benchmark and seasonal revisions.

If revisions meaningfully alter the level or trend of past job growth, markets can treat the report as a structural repricing event rather than a single-month data point. That’s why our “largest surprise” ranking puts payrolls first: the combination of headline + revisions can create fat tails in the rates and FX response.

How Markets May React

A helpful way to think about tomorrow is “rates first.” The front end and belly of the Treasury curve often lead the reaction, and FX follows. Broadly:

-

Stronger than expected (NFP ≥ 100k and/or UR 4.3%): yields up, USD firmer, risk assets choppy; gold typically pressured.

-

In-line / ‘Goldilocks’ (around 60 – 90k, UR 4.4%): risk appetite steadier, USD mixed, yields stable-to-lower depending on wages and revisions.

-

Soft base-case (our call: 45k, UR 4.5%): yields lower, USD softer (especially vs JPY/CHF), gold bid higher; equities may wobble then stabilize if recession fears don’t take hold.

-

Downside shock (≤ 0 – 20k and/or UR 4.6%+ and/or big negative revisions): risk-off response; yields drop sharply; USD becomes more nuanced (can weaken vs havens but hold vs high-beta FX).

Conclusion

Our base case is a soft but not disastrous jobs report: NFP around 45k versus the street at 70k, and unemployment ticking up to 4.5% versus 4.4% expected.

The bigger risk is not a dramatic collapse in the labor market, but a continuation of the cooling trend, amplified by revisions, forcing markets to reprice the Fed path.

In a week where inflation data is still ahead, tomorrow’s print is less about one number and more about what it says about momentum.

This analysis is for informational purposes only and does not constitute investment advice. Trading involves risk; manage exposure accordingly.

For similar Forex Markets news please visit our Markets News page.

Please visit our Disclaimer page.

Disclaimer

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these or any financial instrument or instruments.

TerraBullMarkets.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets or any financial instrument involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress.

All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of TerraBullMarkets.com nor any of its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

TerraBullMarkets.com and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. TerraBullMarkets.com and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and TerraBullMarkets.com are not registered investment advisors and nothing in this article is intended to be investment advice.